What is Cash Book Definition, Explanation and Format of Cash Book

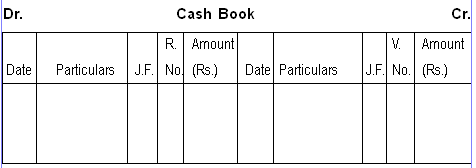

Cash Book

What is a Cash Book

Cash book is a original book of entry where cash receipt and cash payments entries recorded in detail.

Vouching of cash book

Cash book is a very important financial book for a business concern. The chances of misappropriation of cash are very high that is why auditor has to see that no receipt or payment of cash is unrecorded in cash book.

Cash Book Entries

| Debit Side Or Receipt Side | DR | Credit Side or Payment Side | CR |

| Cash Receipt A/C | 10 | Cash Payment | 10 |

Receipt or Debit Side of Cash book

The technique of vouching in respect of the important items which usually appear on the debit side of cash book is discussed here

Cash Sales

The required evidence for vouching the cash sales would depend upon the procedure for recording cash sales in the book the following points are normally considered by an auditor

Auditor should examine the effectiveness of system of internal check in operation in regard to cash sales

If agents are appointed to collect rent the statement of accounts submitted by them should be checked.

He should thoroughly check the carbon duplicates of cash memos with summaries of cash sales.

All receipts and receipt books should be separately and consecutively numbered.

All receipts are printed forms.

Distinction should be made between cash discounts and trade discounts because trade discounts should be entered in books at net value of sales.

The basis of charging prices to customers against cash sales should be examined.

The receipts have to be signed be a responsible officer.

The unused receipt books should be kept in safe custody with some responsible officer.

Bills Receive able

The amount received against bill receivable should be vouched with reference to bill receivable book

Whereas bills maturing in next year and discounted with bank should not have effect in balance sheet.

If bill is maturing in current accounting period then amount received should immediately be recorded in cash book and bill receivable book

Rent Received

Lease deeds and agreements should be examined to ascertain the amount of rent the due date and provision regarding repays.

The counter foils of rent receipts issued to tenants should be checked.

If agents are appointed to collect rent the statement of accounts submitted by them should be checked. If you have a house and you want to rent your house, you must do agreement to renter about rent and advance payment of house rent. you must signature on above format and take and give him detail of rent. Rent Received entry in cash book is debit side. Because payment received.

- Receipt from Debtors Or Credit Sales

For vouching receipts from debtors the following steps should be taken.

Vouch all cash receipts from debtors with counterfoils or with copy of invoice.

If carbon copy of invoice is available then amount should be reconciled with cash book and customer’s record.

Auditor should check that proper steps have been taken by management to uncover the process of teeming and lading or lapping.

Amounts and rates of discounts should carefully be scrutinized.

Auditor should pay special attention to discount allowed to customers for prompt payments

He should also keep a check on bad debts written off.

Bank reconciliation statement should be checked if customers are regularly depositing the money into bank account.

- Commission Received

Counterfoil is carbon copy of the receipt should be checked with the amount in cash book.

Agreements with agent can also make clear the rate and amount of commission so these agreements should be studied thoroughly.

Calculation of amount received and the basis of the working should be checked.

- Interest Income

If company has deposited money to fixed deposit account then bank FDR i.e. deposit Receipt should be checked to confirm the rate of interest and principal amount.

Bank Pass book is the evidence to confirm interest amount on deposit in other accounts.

Interest on any loans granted should be vouched with reference to agreement with the borrower.

Interest on particular fund should properly be credited to it with exact amount for example interest on provident found must be credited to that found only.

If interest comes from securities than vouching of such income should be made from a schedule obtained from some responsible official.

- Dividend Income

For Receipt of dividend these vouchers should be seen:

- Counterfoils

- Dividend Warrants

- Letters Received along with cheques

On Amount of dividend, Withholding tax is deducted on behalf of tax department.

Auditor Should ensure that all such income whether received or accrued has been accounted for in the books of shown inBalance sheet.

- Sale Of Investments (Bonds, shares etc)

Investments are usually sold through brokers so brokers sold note should be examined to vouch the cash received from sale of investments.

The brokers sold note contains detail about.

- Actual Amount Received

- Commission paid to broker

Often Securities are sold at Ex-dividend, cum-dividend.

So auditor should carefully examine the matter

If sale has been affected through back then bank advice should be a source of vouching bank advice contains

- Principal Amount

- Dividend Amount

- Sale of Fixed Assets

No fixed asset can be disposed off without the permission of directors.

The sales contract is the basis of entries in the books of accounts.

A fixed asset is sold through a broker or Auctioneer so brokers Note or Auctioneer, Note should be examined.

It is also noted that any profit so earned show be credited to capital reserve A/C and not to the General Profit and loss Account.

The Auditor Should see that sale has been duly Auctioned.

- Subscriptions Received

In case of non trading Concerns like clubs, schools, hospitals, and welfare institutions subscription is the main source of income.

The income received on account of subscriptions can be vouched with the help of register of subscriptions and counterfoils of the receipts.

The only amount which is received as subscriptions should be in cash book.